Cash flow problems rarely announce themselves. They creep in quietly, like a delayed customer payment or unexpected equipment repairs. Before you know it, you’re staring at a healthy revenue report but wondering why your bank balance doesn’t reflect your hard work.

As partners to inventory-heavy business owners, we’ve seen this cycle. You’ve got capital locked in products on shelves while the bills arrive like clockwork. The gap between paying for inventory and collecting from your customers creates cash flow pressure.

Don’t just work harder or hope for better months. The solution is to take control through a 90-day cash flow plan.

A 90-day horizon gives you the perfect planning window. It’s long enough to see patterns and anticipate challenges, yet short enough to forecast accurately. For businesses carrying inventory, this timeframe typically:

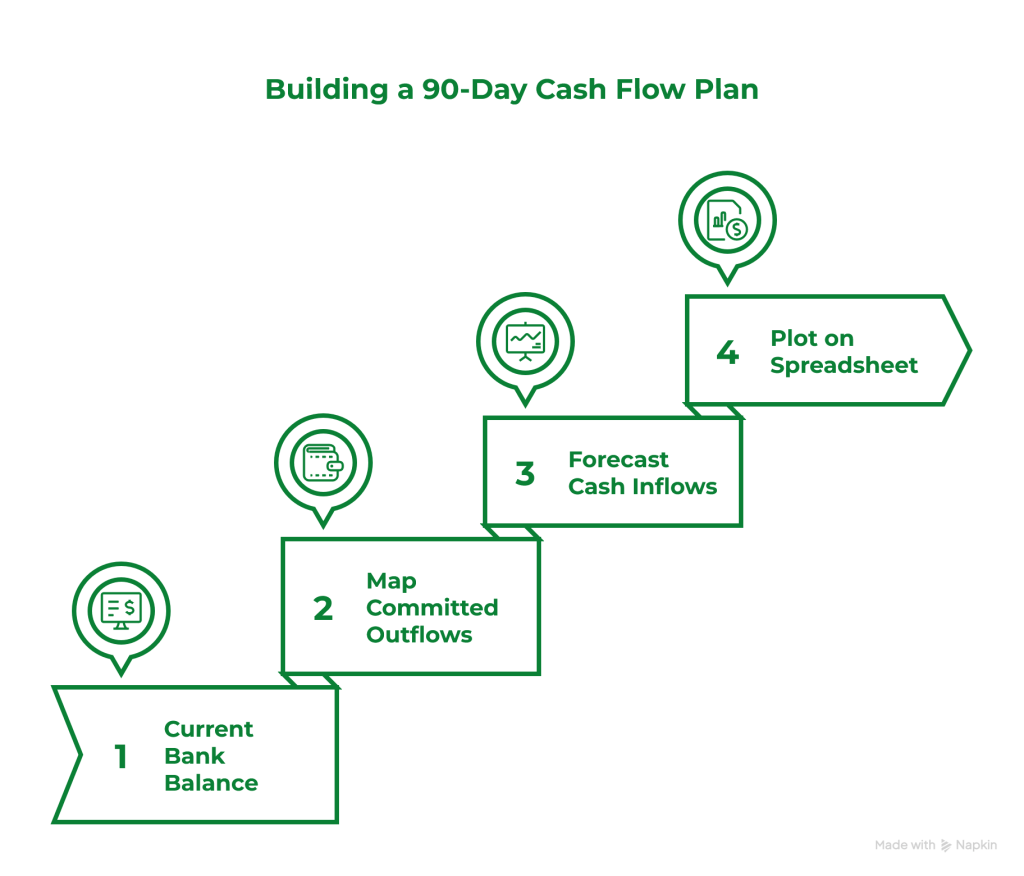

This is day zero of your plan. Forget what your accounting software says you should have on paper. Look at the actual cash sitting in your accounts right now. This is the starting point for every decision you’ll make over the next three months.

2. Map your committed cash outflows for the next 90 days

Next, look at your non-negotiables. These are the payments that keep the lights on and your team happy.

3. Forecast your cash inflows

Review your accounts receivable based on actual customer payment patterns rather than the due dates on your invoices.

If a client typically pays in 45 days even though your terms say 30, plan for 45.

When projecting new sales, it’s better to be pleasantly surprised by an overage than stressed by a shortage. If you usually collect 60% of your revenue in the first month and 35% the following month, use those numbers.

4. Plot everything on a simple spreadsheet with weekly or bi-weekly columns

Watch for the valleys—periods where outflows exceed inflows. These danger zones need attention now, while you have time to:

Your 90-day plan reveals where cash gets tight before it happens. Maybe you discover that planned spring inventory purchases will drain your checking account two weeks before your largest customer typically pays.

Now you can address it. Negotiate payment terms, delay non-critical purchases, or plan a temporary line of credit draw.

The power isn’t in creating a perfect forecast. It’s in having visibility to make informed decisions instead of reactive ones.

Building and maintaining a dynamic cash flow plan takes time and expertise many business owners don’t have. Our fractional CFO services take this burden off your plate while giving you better financial visibility than you’ve ever had.

We create detailed cash flow projections tailored to your industry’s unique cycles and develop realistic budgets that account for inventory demands. We also establish KPIs that help you monitor financial health in real time.

Stop reacting to cash crunches. Let’s build a proactive financial management system that gives you confidence and control. Contact us today to discuss how our CFO services can transform your business finances.

Christine Gervais

Christine Gervais is a licensed CPA, using her skills to help businesses grow and achieve their fullest potential. Christine has a Master’s degree in accounting from Southern New Hampshire University in addition to holding her CPA license for over a decade. Notably, Christine is a nationally recognized speaker providing education to other CPAs on how to best serve clients as well as instruction on a wide variety of topics for business owners on how to maximize success. Christine prides herself on the value she can bring to clients with her extensive tax knowledge and provides strategic, forward-thinking financial strategies to help clients grow. When not behind her desk, you can find Christine spending quality time with her daughter and stepson or tending to the family’s excessively loved farm animals.